Fishing Scams: Bigger, Longer, and Uncut!

Readers' mail is one of the things I enjoy the most. People from all corners of the world get in touch to ask about tackle, share their experiences, send me trophy photos, and share whatever gossip and bits of news they hear. Unfortunately though there are times when I get upset over emails. Nope, not the hate mail, I enjoy this because it tells me I'm making a difference. Rather it's when I hear from someone who got scammed buying tackle. In most of those cases there is nothing that could be done except consoling them, so I decided that instead of sitting idle I should post a few tips about the various scams in hopes that this would help some fishermen avoid being ripped off. If you find it useful help spreading it and make sure everyone you know reads it.

The dodgy tackle shops

I will begin with this because it's the most effective way that thieves use. This is basically a scammer setting up a fake online tackle shop then waiting for victims to fall prey. I will use an actual example to demonstrate how these scams work and how to spot a fake shop. I will use screen captures because these sites disappear and reappear and I don't want to put links that eventually stop working.

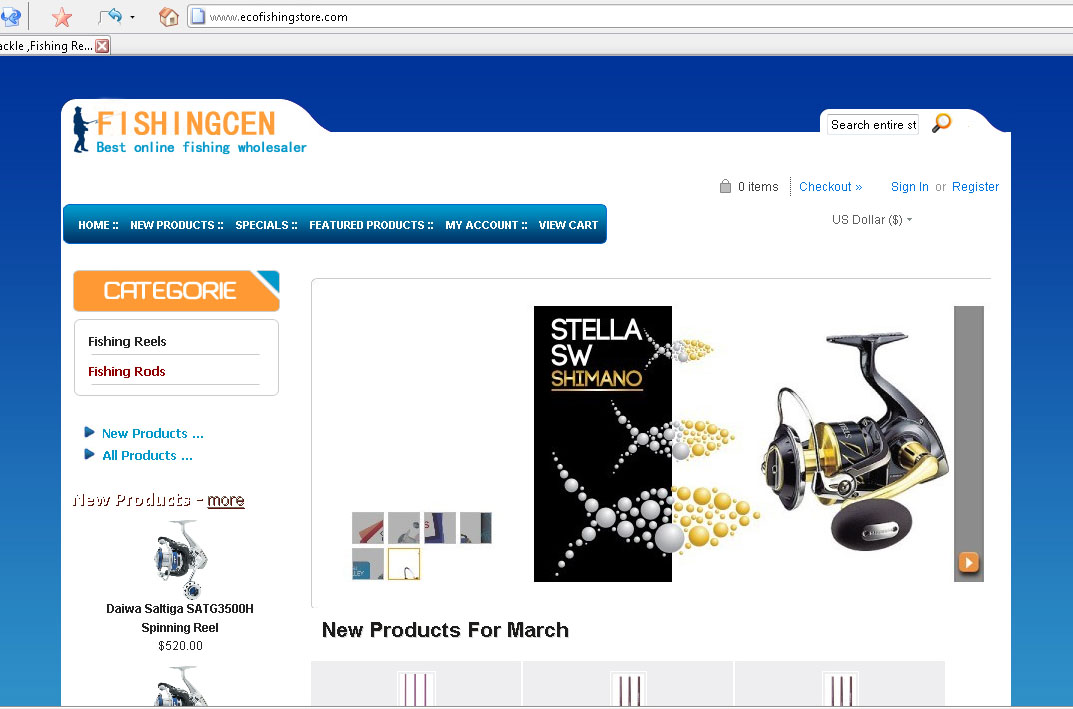

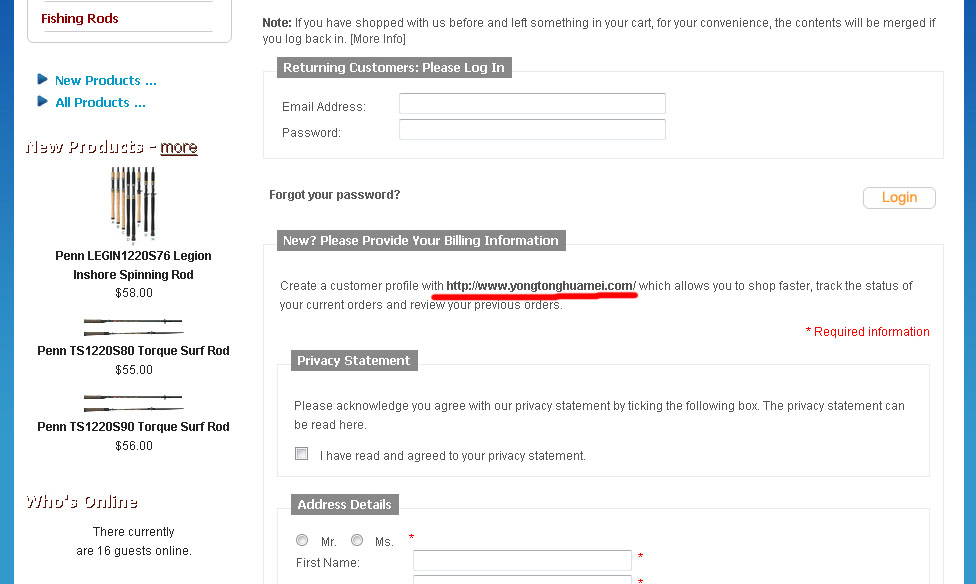

This is the main page of such site. As you can see high end reels such as Saltigas and Stellas are featured to lure in buyers.

First thing to tip you off is the very low prices, which is a constant because that's how they lure the victim. If they didn't discount items there would be nothing to convince or tempt you to try them. This crook is reducing the prices by about 40%-80%, but smarter ones would discount them by only 15%-20% to make it more believable.

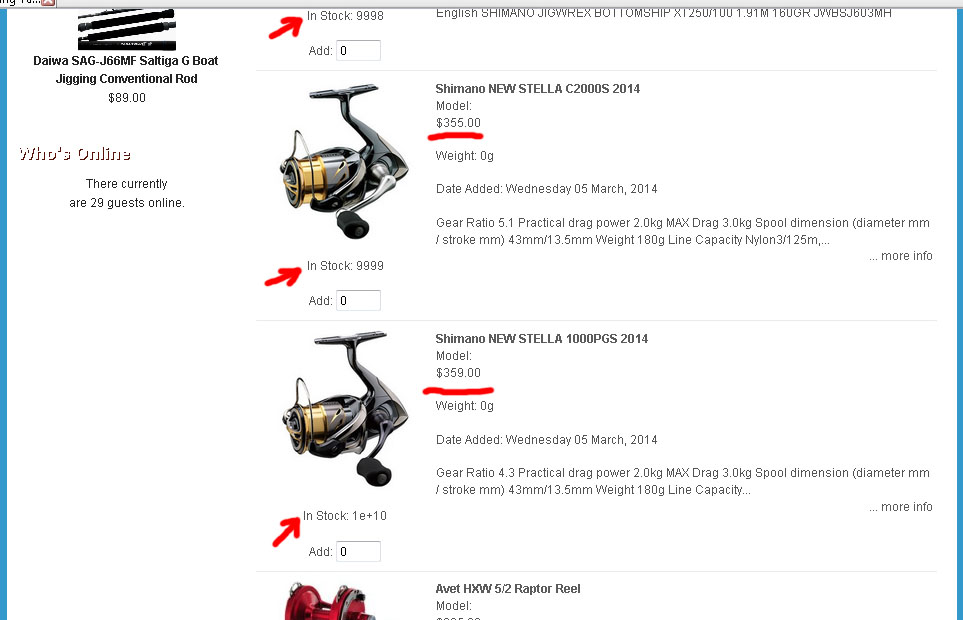

Still in the above photo, the second clue that it's a scam is that everything is always in stock. That's rubbish of course because even reputable premium tackle shops would not have everything in stock all the time, so how could you believe that some obscure shop would have every single item ready to ship? Common sense states that a scammer should list some items as "out of stock" to make it look real, but their greed makes them list everything as "in stock" because they wouldn't risk losing a victim who wanted an item that they listed as unavailable.

Another clue is the contact information. When you click the "contact us" link on those fake sites, you get a web form that sends your question to the scammer's email, but you don't get a physical address with a phone and fax numbers like you would expect from a real shop. Of course they could put a fake address, and they sometimes do, but in most cases it's just a web form and a mobile phone number without a physical address.

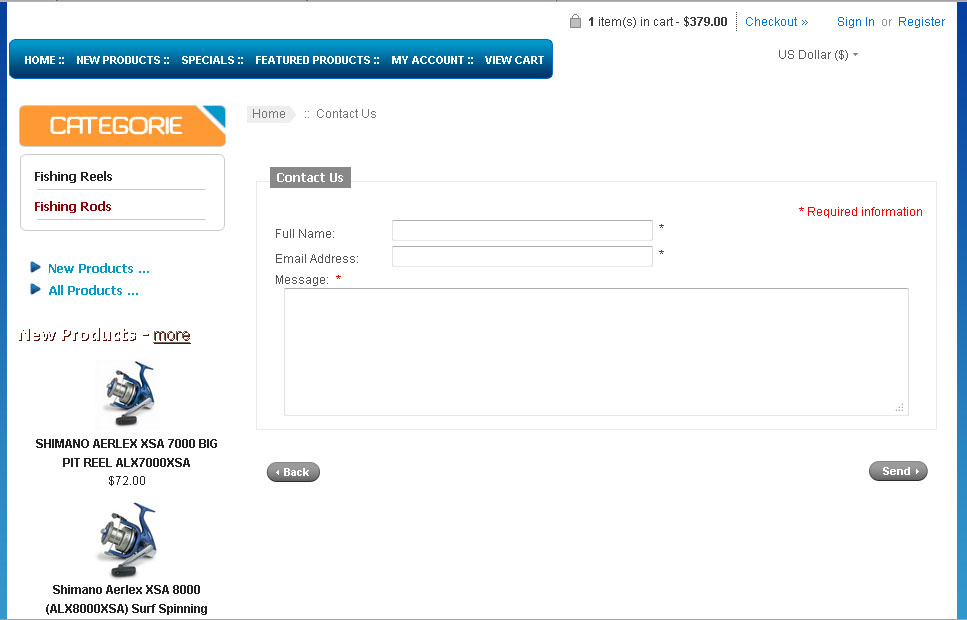

The biggest clue of all though is how they actually take your money. I'll place an order and proceed with the check out to show you what comes next

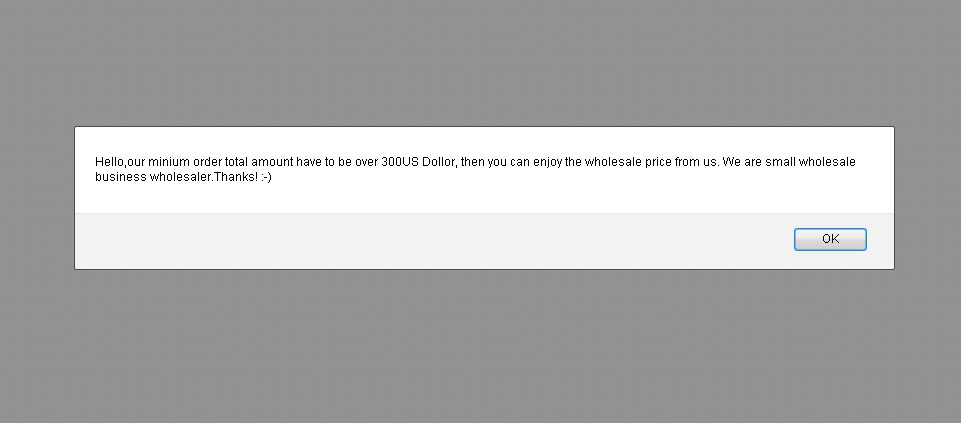

This is one of the few tricks they do to fool your mind into believing the very low prices. I put a $185 reel in the basket and wanted to proceed, but I got this error message stating that they need every order to be $300 or more because that's what makes it possible for them to offer those low prices. Ya, right, I almost stopped writing this article and placed an actual order because it convinced me! Just kidding, but unfortunately people looking for a bargain don't see through this and lose money.

This moron made a funny mistake: he used to have a different name and web address for his fake shop, then when he had to change name and move he forgot to edit this bit leaving the old name and web address! They usually are forced to move when they have scammed a few people and those people start writing about it online, so the scammer changes name and web address to avoid being exposed by the warnings posted by victims.

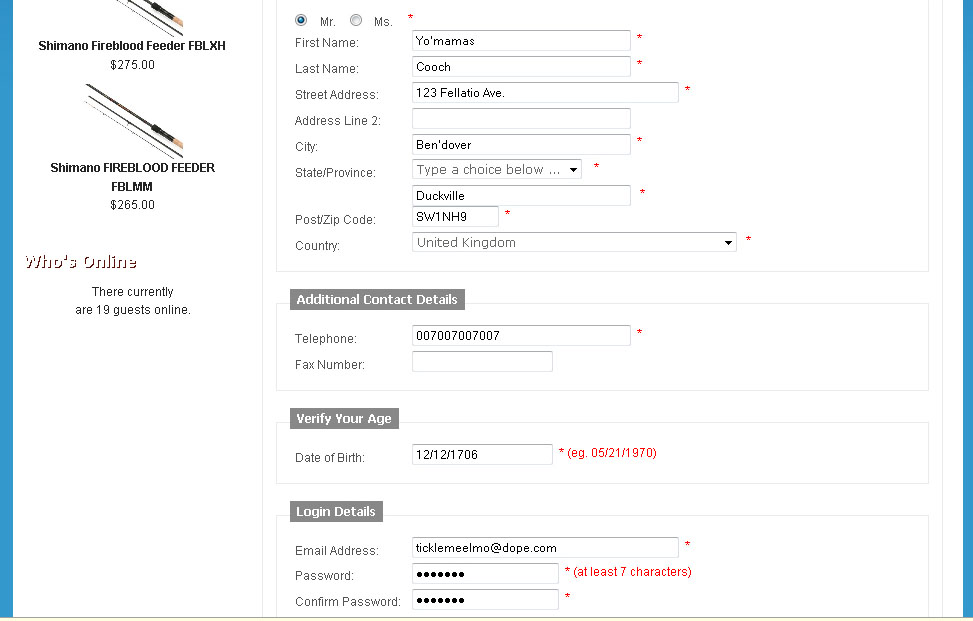

Proceeding with the order and entering fake information of course because I want to arrive at the payment page.

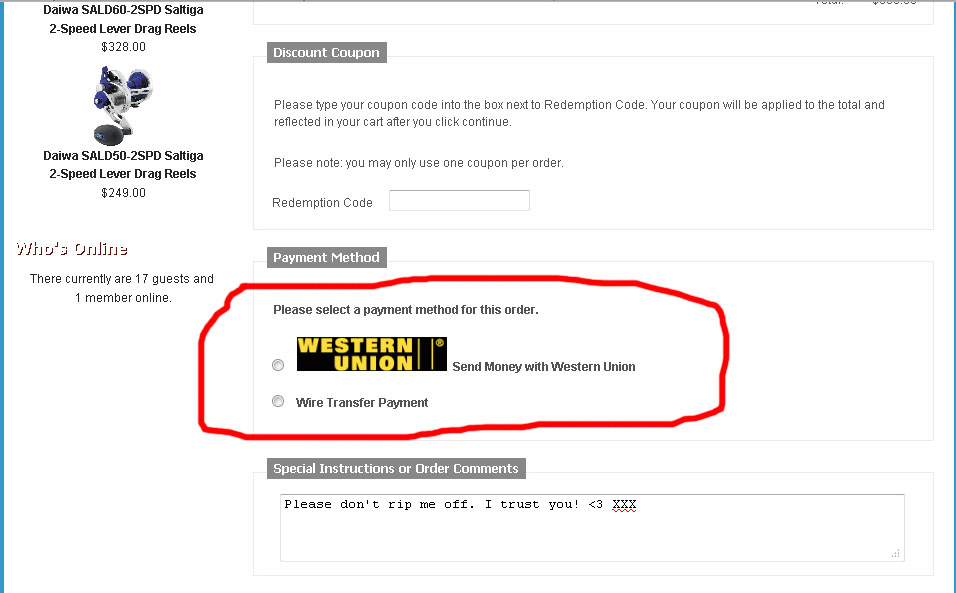

Here it is! The payment options are either wire bank transfer or instant transfer via companies such as Western Union and Money O'Gram. In almost all countries there are banks that let people open an account using fake information and without checking an ID or national security/insurance number, and these banks mail them an ATM to whatever address they enter which is always a rented apartment. When a victim wires the money to this bank account, the scammer will withdraw it using the ATM card without ever risking walking into the bank in person, and they keep doing it until someone complains and the account is closed so the scammer would start all over again. Instant transfer companies such as Western Union is even better for the scammer because they just need you to give them the receipt number (Money Transfer Control Number) and the secret word that you typed when you sent the money. They go to a local office and give the cashier the number and the secret word and walk away with your money without needing to show an ID.

Over the years I saw sites that would put Paypal logo as an accepted method of payment, then when you proceed with the order you never get a Paypal option and you only get the bank wire or Western Union/Money O'Gram options. Paypal makes it hard to steal your money so scammers tend to avoid it, but that doesn't mean Paypal is fool proof as I will discuss later on when I speak about Paypal scams. Also sometimes the scammer would have a Credit Card payment option, and this is even worse because instead of just stealing whatever you intended to pay for the imaginary tackle, they take your card's information and use them to buy stuff for themselves until your card is maxed out, then they disappear. Your card could also be used to purchase illegal goods (steroids, underage pornography, pirated digital material) so instead of only suffering financial loss you could face criminal charges and have your reputation ruined as you fight to prove that someone else was using your card for the illegal purchases. It happened before.

Another way to figure out scam sites is by doing a whois lookup. I'll use the same site above to show you how it's done and what to look for.

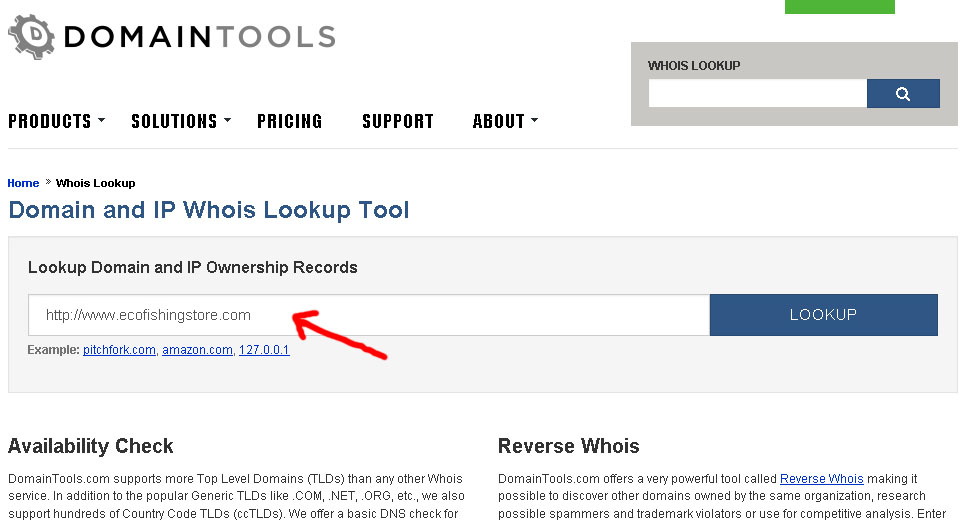

There are several whois search engines. We are using http://whois.domaintools.com for this example. You enter the suspect site's address in the box and hit the search button, and examine the result that comes up

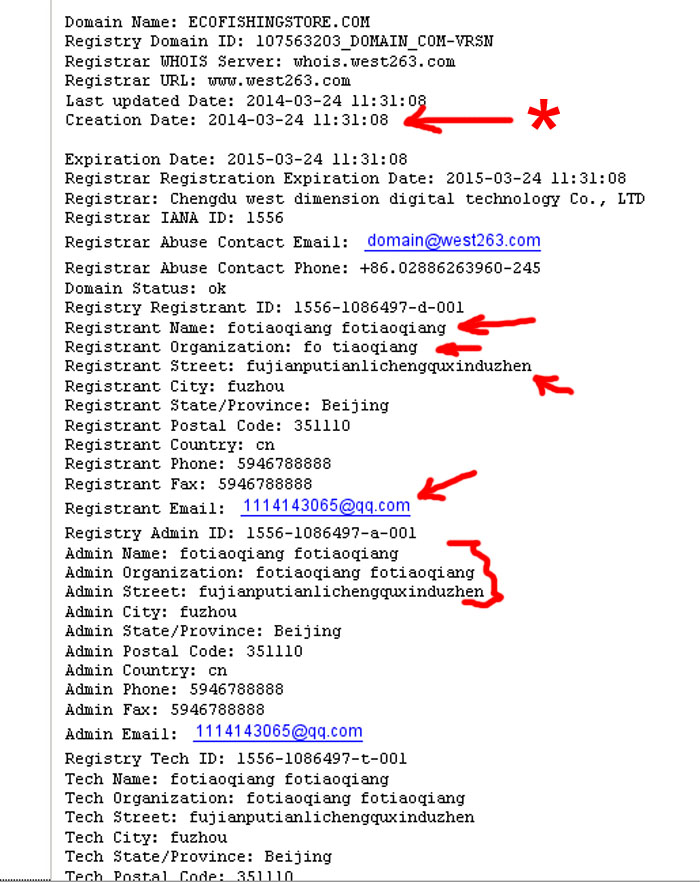

The first and most important clue is the "Creation Date". This web address was created on March 24th 2014. That's a scam site's trademark. They are always at recently created addresses, and while this one is just days old some of them would be a few months or even a year old. It's hard for those sites to survive any longer and a new address would be needed when people complain. Also I pointed the rubbish name, address, and email by the arrows. A real tackle shop would not be owned by Mr. "Fotiaoqian" who lives in "Fujianputjyesrkdshfjhfdertt"! A scammer could still enter a proper fake name and address here, but this one helped a lot by entering these random keystrokes.

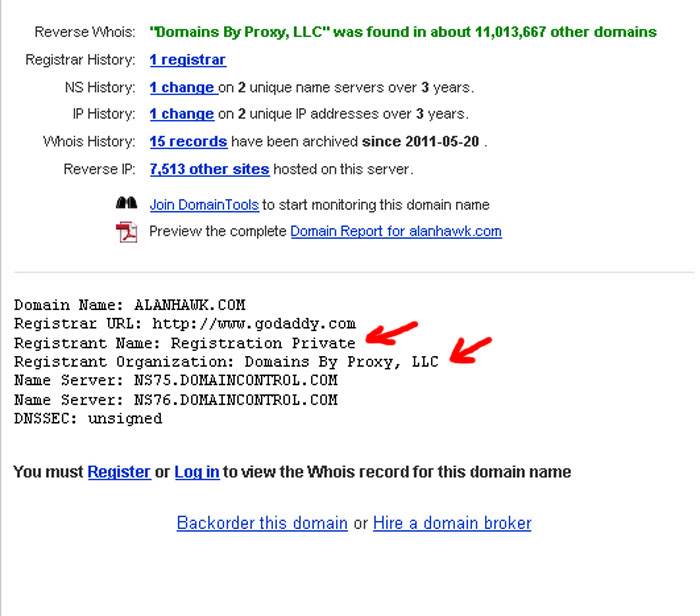

Something else that I've seen in the past is private registration. I don't know any fake shops that are still online who use this method, so I will use my own site to demonstrate.

Private registration doesn't show the owner's private details, and instead it states that it's a private registration. This type of registration is something that sophisticated fake tackle shops use sometimes when they fear that someone might look them up and see that the information doesn't make sense. Private individuals who don't sell anything would choose a private registration to keep their home address and phone number away from spam engines and marketers, but a company or a business would not keep its information private because it's a public establishment whose information is available to everyone, and they would actually want their information to be spread not hidden. So a tackle shop with a private registration is a big warning sign.

Before I leave this type of scam, I need to say that the above are just examples of clues that should warn you that something is wrong. 99% of scam sites would show one or more of these warning signs, but there are still some really tenacious people out there who will work hard and cover their tracks in order to rip you off. For example I once saw a scam tackle site whose owner bought the web address and left it unused for 4 years, so when he moved the scam shop to that address it came in the whois search as a 4 years old site. Ultimately your brain is the most effective tool to fight scams, and you should always be vigilant and follow this golden rule: "If in doubt, don't". I use it for everything in my life and even though it's not perfect it generally is a safer policy than others.

Ebay

Ebay is a whole different game for the scammers. Those who do the fake tackle shop scam can sit and relax and receive many small orders worth $200-$400 over a period of time before they become known and orders slow down, and because they are usually located in countries such as China, the web providers hosting their fake sites are non-responsive to complaints and usually are slow to take action. When dealing on Ebay though the scammer can't list the same huge number of objects, also Ebay is quick to respond to suspicious activity, so the scammer would want to sell expensive reels very quickly before he is caught. The large majority of fishing tackle scams on Ebay are of reels priced at +$500, with Stellas and Saltigas being a favourite target since they are way more popular than large multipliers or electrical reels.

Spotting a scam on Ebay is less complicated and requires a few clicks and a sharp pair of eyes. Click on the seller's profile and look at his history. As a general rule you should stay away from newly registered sellers without a track record. Being a new seller does not at all mean that they are up to no good, but do you really have to buy a $1000 reel from someone who signed up last month? If he is selling the reel at the average market price, then why don't you go to one of the established sellers since the price is close? And if the new seller is listing the reel at a considerably discounted price, then it's even more reason for you to be suspicious and look somewhere else.

If the seller is an old ebay member and have a lot of feedback, then look through the feedback he received as a seller from buyers. Check the dates of the feedback he received and see if it's recent or not. If the seller's account appears to have gone cold for a period before becoming active again, then it could be a legitimate account that is now hijacked by a hacker who is using it to defraud people. Also look at the nature and price of items sold recently for which he received the feedback. Someone who received feedback for selling many little items worth $5 or $20 and is now suddenly selling $1200 reels should ring an alarm bell in your head. Finally, even if the seller seems to have received positive feedback for selling expensive fishing reels recently, just look at the happy buyers' feedback and see how many feedback each has. If you see several positive feedback entries made by buyers who have 1 or 4 feedback records, then those happy buyers are most probably fake accounts made by the original scammer in preparation for the big hit when he would sell 5 or 10 reels worth $1000 each then run away with a fortune. The above sounds complicated, but read it again and you'll see it's all a quick check that takes no more than 30 seconds to establish if the seller is genuine.

Ebay listings would have Paypal listed as a payment option and the scammer will have to follow that rule, but when you read the description you will find that he asks for the payment via Western Union, Bank Wire, Cashier's cheque, or money order, or he would not say anything but after you buy he will make up a story about why he can't use paypal and ask you to send the money using one of those dangerous payment methods. He would entice you to do that by offering further discount or free shipping, or he would try intimidate you by saying he would file a non-payment complaint with Ebay to hurt your standing. If a seller who lists Paypal as a payment method refuses to use it and tries to intimidate you into sending money some other way, send him a photo of your toilet right before you flush, then forward his emails to Ebay so they can kick his butt.

Paypal

This is one of the safest payment methods available, but it's not a green light for you to go about making risky purchases just because PP covers you. PayPal is ultimately about making money, and if you got defrauded they will reimburse you once or twice and maybe trice, but if you get scammed a handful of times they might deem you a high risk person and limit your account. You don't want that to happen, and you don't want to go through the hassle involved in making a claim for a refund, so you better think before you pay.

There are transactions that are not covered by Paypal though, where you don't get any sort of refund even if it's your very first claim. These are "gift" paypal payments which are sometimes used to complete sales on web forums and fishing chat rooms. Sometimes a seller would ask for a gift paypal payment to avoid Paypal's 3% charge so he can offer you a lower price, and while this would appear to be a win-win situation for both seller and buyer, it could end up costing you much more if the seller is dishonest. Gift payments are like sending someone cash and is something that should only be done if you know the person and fully trust them.

When you pay someone using gift paypal you don't only run the risk of never receiving the item, but you could also receive something that is defective or not as described. Unfortunately most sellers think it's fine to embellish and claim the item is in a better shape than it actually is, or say the biggest lie of all which is "only fished once", and they think it's smart or crafty to do so. Actually anyone who intentionally misrepresents the condition of an item even very slightly is nothing more than cowardly lowly thief who would also shoplift if he weren't too afraid of being caught. Some people think it's harmless to lie about little things when describing the item, but they wouldn't be happy if that happened to them so it's fraud no matter what they tell themselves. As long as people still act like that every day, you shouldn't deny yourself the ability to reject a misrepresented item and get your money back.

So sum it up, unless you can fully trust the other person don't send a gift payment and just pay the 3% and make it a commercial payment. On a $400 item that 3% is just $12, and for a $900 items it's $27 which is the cost of a quick lunch for two. Again I'm not saying that everyone who is asking for a gift payment is up to no good, but if they aren't people whom you know and absolutely trust, offer them to pay the fees yourself and make it a commercial payment, or just move on to someone else who accepts the commercial payment.

Card payment and general advice

There are two types of cards, credit and debit. Debit cards take money direct from your account, and if the card's information falls in bad hands you could lose everything you have in that account. Fraud protection for debit card is pretty weak and you will really suffer to recover your money because no one cares, so NEVER EVER use your debit card online, and an even better option would be not to have a debit card at all because if your wallet is lost with the debit card you could be devastated financially. If you must have one, open a new account where you leave $500 maximum and get a Debit card for it so you can get small cash for taxi or restaurant tips on a night out. Credit cards though are fully protected and a bank would pay you back any money you lost fraudulently and give you a new card with new details upon request. Like paypal though, too many fraud claims and your bank might cancel your card. So also use with care.

The way we use our credit cards to buy tackle is usually by calling a known shop and giving them the card's details, or by entering the details online while we place an order from a trusted shop, and problems are very rare. Still, before you use your credit card you have to be aware of something that's called "charge back period". A bank or a credit card issuer offers you a period during which you can file for a "charge back", which is the reversal of a payment you made using the credit card and restoring your money to you. This period ranges from 40 to 180 days from the time of payment (or time you became aware of the problem for some cards), so check with your bank or issuer to figure out the exact time frame.

Buying from places such as Cabela's, Bass Pro, Amazon, etc. is never a problem, but problems could come when dealing with smaller shops, especially when you back-order an item that is not available in stock. A few years ago a tackle shop in the USA who used to be alright went through a phase where they were taking orders and charging peoples' credit cards, then telling them that items are delayed or that they are temporarily out of stock and are coming back soon. People would wait and wait and hear all kinds of stories and promises, and eventually tens of customers lost their money when the shop hit the dust! Their mistake was that they waited beyond the "charge back" period, so they couldn't file for a charge-back and were only left with the option to sue to get their money. Since most tackle orders are worth a few hundreds at most, a costly legal action isn't always a good choice. So in order to be safe when using a credit card, make sure you know how many days you have as a charge back period, and if the merchant still haven't delivered your goods within 15 days of the expiration of the period, tell them to refund your money immediately or file a charge back with your bank/issuer. If you trust the merchant and you know that your item is delayed for a genuine reason, you should still ask them to refund your money then ask them to make a new charge on your card so you would have a fresh period in which you can file for a charge back if the item is still not delivered.

Finally, I consider it some form of scam when you receive an item that is wrong, defective, or not as described, then the shop tells you to send it back for a refund or replacement and doesn't give you the money you spent to send it back. You don't have to accept that, and you shouldn't accept it as a matter of principal no matter how small the amount is. If the return is because you changed your mind or had a buyer's remorse then of course you should pay for the return, but if it's the merchant's fault then they should pay you back the return cost. If they refuse then threaten them with a chargeback and go ahead and do it, and sometimes the special department in your bank would take the item from you and after they take the money from the merchant and give it back to you they will tell the merchant to come pick up his goods or pay for their return if he still wants them! If enough of us did that merchants should learn to act fairly and responsibly and to stop charging people for no fault of theirs.

Note that when you do a charge back and receive credit the merchant could sometime make counter claims and reverse the action, but you then appeal and have the refund reinstated and by then the merchant is left with the expensive and risky arbitration option and they usually surrender at that point if they are originally at fault. Study the rules of charge back by your issuer to be familiar with the time, limits, rules, and anything else there is to know.

That's all. Know your rights, act smart, firm, and fair, and you should be safe buying tackle (or anything else) online.

Cheers

Was this a good read? Please click here

Alan Hawk

March, 29th, 2014

|